UK KYC compliance has become a critical requirement for banks, fintech companies, payment providers, crypto firms, and regulated businesses operating in the UK. Rising financial crime risks, stricter AML regulations, and the rapid growth of digital onboarding are pushing businesses to strengthen identity verification, customer due diligence, and fraud prevention processes in 2026.

According to the UK Finance Annual Fraud Report, criminals stole more than £1.1 billion through fraud in recent years, increasing pressure on businesses to improve AML screening, sanctions checks, and customer verification workflows. Strong KYC compliance helps businesses reduce onboarding fraud, detect suspicious activity, and meet FCA compliance requirements.

This complete guide to UK KYC compliance for 2026 covers UK AML regulations, digital identity verification, onboarding workflows, customer due diligence, enhanced due diligence, compliance challenges, penalties for non-compliance, and best practices for building secure and scalable compliance operations.

Binderr UK KYC Compliance Software

- Biometric face matching and liveness detection for fraud prevention

- OCR data extraction for faster onboarding and customer verification

- AML screening across sanctions lists, watchlists, PEPs, and adverse media

- Dynamic risk scoring for customer due diligence and enhanced due diligence

- Ongoing AML monitoring with real-time compliance alerts

- API-based onboarding workflows for scalable compliance automation

- High-accuracy verification with low false positives and faster approvals

What is KYC Compliance?

KYC compliance, also known as Know Your Customer compliance, is the process businesses use to verify customer identities, assess financial crime risks, and prevent illegal activities such as money laundering, fraud, terrorist financing, and identity theft. UK-regulated businesses must follow strict KYC and AML compliance requirements to ensure customers are genuine and financial transactions remain secure.

Customer verification is a core part of UK KYC compliance and includes identity verification, proof of address checks, biometric authentication, sanctions screening, PEP screening, and customer due diligence. Businesses use these checks to validate customer information, identify suspicious activity, and reduce onboarding fraud risks during digital onboarding processes.

Try Free Binderr Compliance Screening Tool

Why KYC Compliance is Important in the UK

UK businesses face growing pressure to strengthen KYC compliance, AML screening, customer due diligence, and identity verification processes as financial crime risks continue to rise in 2026.

FCA compliance requirements, digital onboarding growth, sanctions screening obligations, and fraud prevention expectations are forcing regulated businesses to implement stronger compliance workflows, ongoing monitoring systems, and risk-based customer verification frameworks.

Prevents money laundering and financial crime - Strong UK KYC compliance processes help businesses detect suspicious transactions, identify high-risk customers, and prevent illegal financial activities linked to money laundering, terrorist financing, and fraud. Customer due diligence, identity verification, sanctions screening, and ongoing AML monitoring strengthen financial crime prevention frameworks and help regulated businesses reduce compliance risks.

Helps businesses meet FCA compliance requirements - Regulated businesses in the UK must comply with FCA compliance requirements, AML regulations, and customer due diligence obligations to maintain secure onboarding and transaction monitoring processes. Effective KYC verification, risk assessments, and AML screening workflows help businesses maintain regulatory compliance, improve audit readiness, and avoid operational disruptions.

Reduces fraud and identity theft risks - Identity verification, biometric authentication, document verification, and liveness detection help businesses reduce onboarding fraud, fake identities, account takeover risks, and deepfake-related threats. Advanced digital KYC verification systems improve fraud prevention while helping businesses verify customers securely during remote onboarding.

Supports secure digital customer onboarding - Digital KYC compliance solutions allow businesses to onboard customers faster while maintaining strong AML compliance and identity verification standards. Automated onboarding workflows, OCR data extraction, biometric verification, and AI-powered fraud detection improve customer experience, reduce manual reviews, and support secure remote onboarding.

Improves AML screening and risk management - AML screening, sanctions checks, PEP screening, adverse media monitoring, and customer risk assessments help businesses identify financial crime risks before onboarding customers. Risk-based compliance frameworks improve compliance decision-making, strengthen ongoing monitoring processes, and support enhanced due diligence for high-risk individuals and businesses.

Protects businesses from regulatory penalties - Businesses with strong KYC compliance programs are better positioned to avoid FCA enforcement actions, compliance penalties, reputational damage, and regulatory investigations. Effective customer due diligence, ongoing monitoring, and AML compliance controls help regulated firms maintain secure operations and reduce exposure to financial and legal risks.

Simplify AML and KYC Monitoring with Binderr

Binderr helps businesses improve AML screening, customer monitoring, and onboarding workflows with automated compliance tools designed for regulated businesses.

- Sanctions and PEP screening for high-risk customer verification

- Adverse media monitoring for ongoing financial crime detection

- Ongoing AML monitoring with real-time compliance risk analysis

- AI-powered risk scoring for customer due diligence workflows

- Fraud prevention workflows for secure digital onboarding operations

- Real-time compliance alerts for suspicious activity and sanctions updates

UK KYC Regulations and Compliance Framework in 2026

UK KYC compliance in 2026 is shaped by strict AML regulations, FCA compliance requirements, customer due diligence obligations, and financial crime prevention frameworks designed to protect the UK financial system.

Regulated businesses must implement strong identity verification, AML screening, sanctions checks, ongoing monitoring, and risk-based compliance processes to meet evolving regulatory expectations and reduce exposure to fraud, money laundering, and compliance penalties.

Financial Conduct Authority (FCA)

The Financial Conduct Authority (FCA) plays a central role in regulating banks, fintech companies, payment institutions, crypto firms, EMIs, and regulated financial businesses operating in the UK. The FCA monitors how businesses manage KYC compliance, AML screening, customer due diligence, fraud prevention, sanctions screening, and ongoing monitoring processes to reduce financial crime risks and protect consumers.

Businesses regulated by the FCA must maintain strong onboarding controls, secure identity verification workflows, effective AML compliance programs, and risk-based compliance frameworks. FCA compliance expectations also include transaction monitoring, suspicious activity reporting, enhanced due diligence procedures, and maintaining audit-ready compliance records.

Money Laundering Regulations (MLR)

The UK Money Laundering Regulations (MLR) establish the legal framework businesses must follow to prevent money laundering, terrorist financing, fraud, and financial crime. These regulations require regulated businesses to implement strong customer due diligence, AML screening, identity verification, sanctions checks, and ongoing monitoring procedures as part of their compliance operations.

The MLR framework requires businesses to apply a risk-based approach to customer onboarding and monitoring. High-risk customers, complex ownership structures, cross-border transactions, and politically exposed persons (PEPs) may require enhanced due diligence, additional verification checks, and continuous monitoring.

Businesses must also maintain accurate compliance records, monitor suspicious activity, update customer information regularly, and demonstrate effective AML compliance controls during regulatory audits and investigations.

Proceeds of Crime Act (POCA)

The Proceeds of Crime Act (POCA) is one of the most important UK AML compliance laws designed to prevent money laundering, financial crime, fraud, and the movement of illegal funds through regulated businesses. POCA places strict obligations on businesses to identify suspicious financial activity, maintain strong KYC compliance controls, and report suspicious transactions that may involve criminal property or money laundering activities.

Regulated businesses must implement effective AML screening, customer due diligence, transaction monitoring, and suspicious activity reporting processes to remain compliant with POCA requirements. Failure to identify or report suspicious activity can expose businesses and compliance officers to financial penalties, regulatory investigations, criminal liability, and reputational damage.

Joint Money Laundering Steering Group (JMLSG)

The Joint Money Laundering Steering Group (JMLSG) provides detailed industry guidance to help UK-regulated businesses strengthen KYC compliance, AML screening, customer due diligence, and financial crime prevention frameworks. JMLSG guidance is widely used by banks, fintech companies, payment institutions, EMIs, and financial service providers to build risk-based compliance programs aligned with FCA expectations.

The guidance focuses on customer risk assessments, enhanced due diligence procedures, ongoing monitoring requirements, sanctions screening, fraud prevention, and secure onboarding controls. Businesses use JMLSG recommendations to improve compliance operations, reduce AML risks, and maintain consistent customer verification processes across digital onboarding workflows.

UK GDPR and Data Protection

UK GDPR and data protection regulations require businesses to handle customer identity information securely during KYC verification, AML screening, onboarding, and ongoing monitoring processes. Businesses collecting personal data for customer due diligence and identity verification must maintain strong data security controls, privacy protections, and secure compliance workflows.

Regulated firms must ensure that customer identity documents, biometric verification data, onboarding records, and AML screening information are stored securely and processed in line with UK privacy laws. Strong data governance practices help businesses reduce cybersecurity risks, protect sensitive customer information, and maintain trust during digital onboarding and compliance operations.

Start Free Compliance Checks with Binderr

Step-by-Step UK KYC Compliance Process

A structured UK KYC compliance process helps businesses strengthen customer onboarding, improve AML screening, reduce fraud risks, and meet FCA compliance requirements more effectively.

Strong identity verification, customer due diligence, sanctions screening, and ongoing monitoring workflows allow regulated businesses to detect suspicious activity early, improve compliance operations, and create secure digital onboarding experiences for customers in 2026.

Step 1: Collect Customer Information

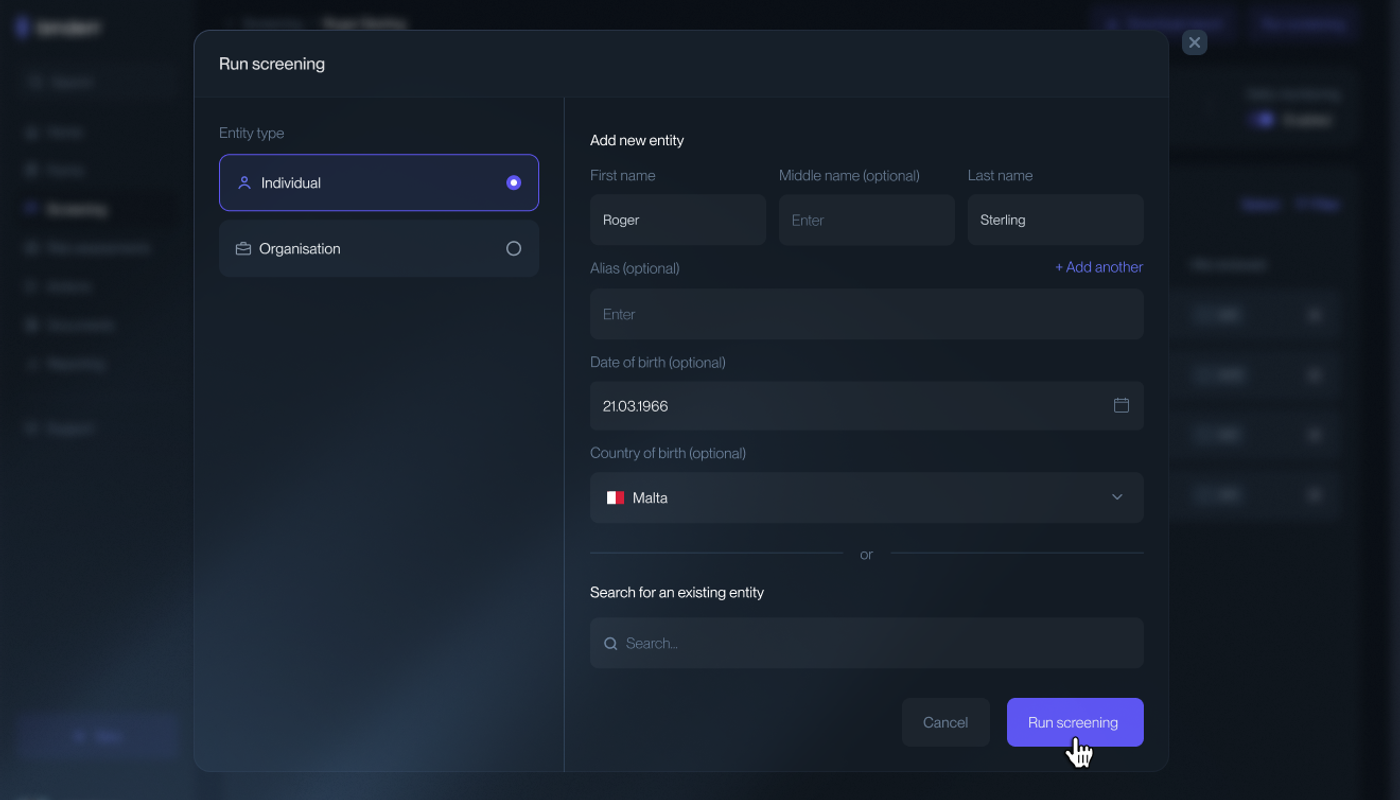

The first step in the UK KYC compliance process is collecting accurate customer information during onboarding. Regulated businesses must gather identity data, proof of address, contact details, business information, and risk-related data to support customer due diligence and AML compliance requirements. Strong onboarding processes help businesses reduce fraud risks, improve identity verification accuracy, and maintain secure customer onboarding workflows.

Businesses commonly collect customer information through digital onboarding forms, automated verification systems, mobile onboarding applications, and compliance platforms. The information collected depends on the customer type, business relationship, transaction risk level, and regulatory requirements under UK AML regulations.

Automated onboarding workflows help businesses collect customer data, run AML screening, and perform risk assessments more efficiently during digital onboarding.

Binderr’s onboarding and screening tools help businesses automate customer verification, AML checks, and onboarding risk assessments from a single compliance workflow.

Step 2: Verify Identity Documents

Identity verification is one of the most important stages in the UK KYC compliance process. Businesses must verify customer identities using government-issued documents, biometric authentication, and fraud prevention technologies to reduce identity theft, onboarding fraud, synthetic identities, and deepfake-related risks.

Modern digital KYC verification systems use OCR data extraction, facial biometric matching, liveness detection, document authentication, and remote identity verification tools to validate customer information securely during onboarding. Automated verification workflows improve customer experience, reduce manual compliance reviews, and support faster onboarding for fintech companies, banks, payment providers, and regulated businesses.

Businesses must ensure identity documents are valid, authentic, and linked to the customer completing the onboarding process. Strong identity verification controls also help businesses meet FCA compliance requirements, strengthen AML compliance programs, and reduce exposure to fraud risks.

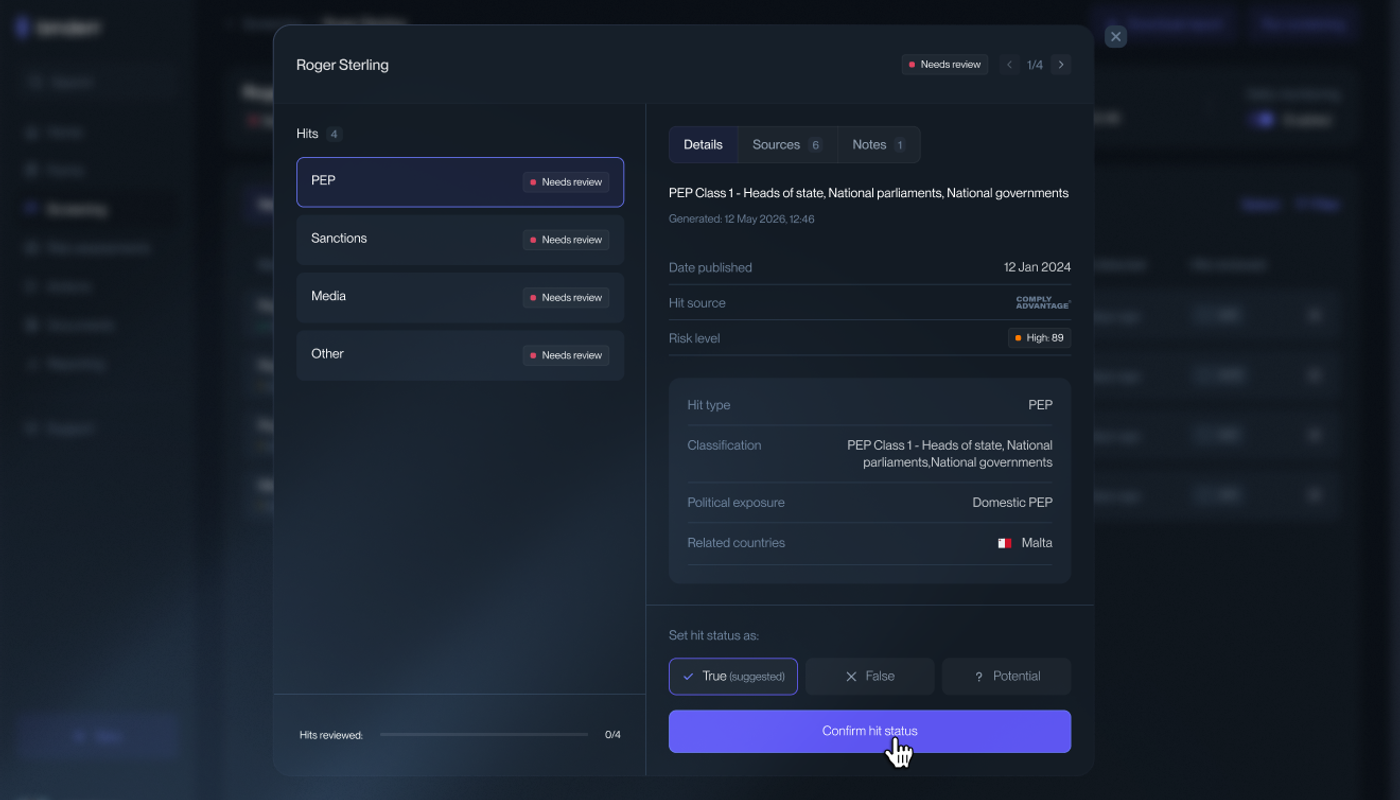

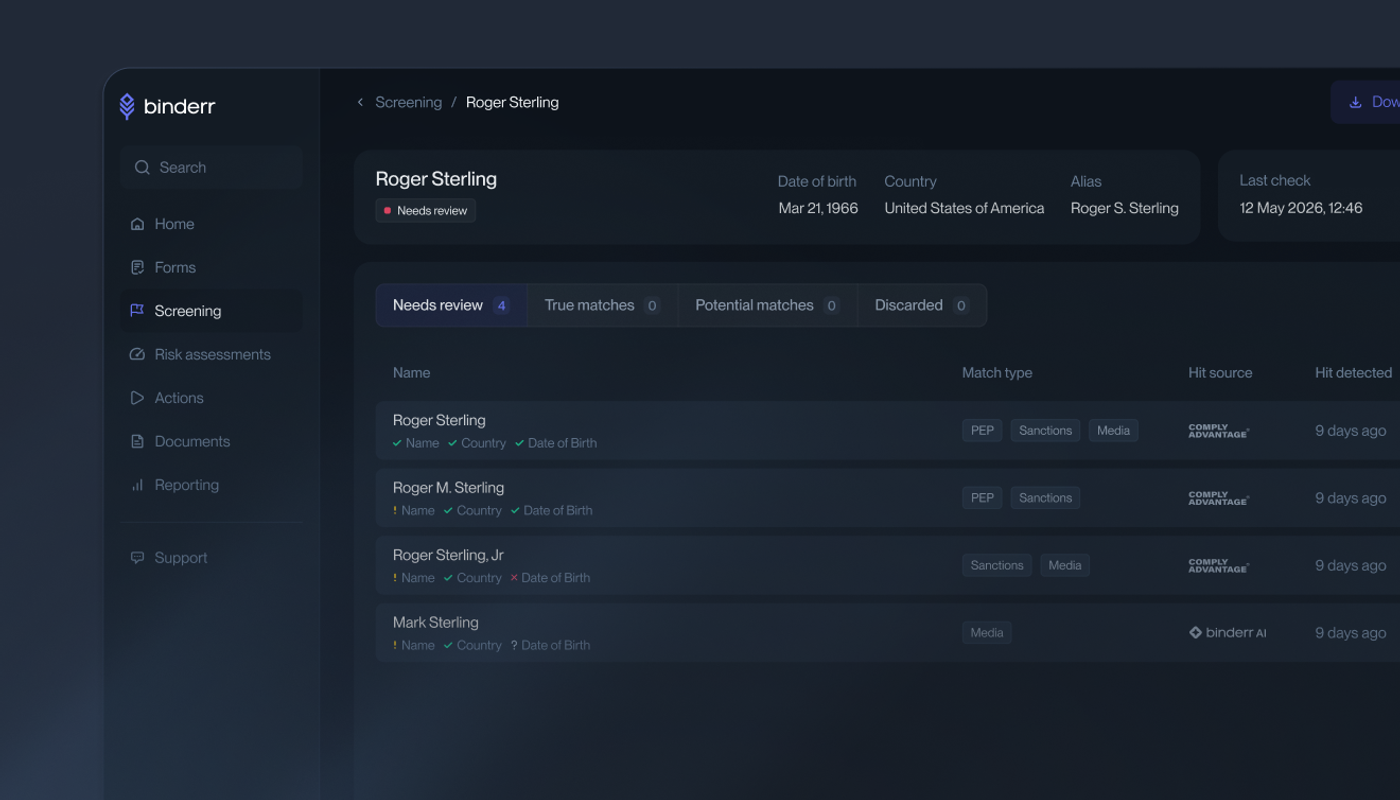

Step 3: Conduct AML Screening

AML screening is a critical part of UK KYC compliance designed to identify high-risk customers, sanctions exposure, suspicious activity, and potential financial crime risks before onboarding customers. Businesses must screen individuals and companies against global sanctions lists, politically exposed persons (PEPs) databases, watchlists, and adverse media sources to strengthen AML compliance operations.

Advanced AML screening systems use automated monitoring, AI-powered matching algorithms, adverse media analysis, and risk-based screening workflows to reduce false positives and improve compliance efficiency. Continuous AML monitoring also helps businesses identify changes in customer risk profiles, sanctions status updates, and suspicious transaction behaviour after onboarding.

Strong AML screening frameworks help regulated businesses improve fraud prevention, maintain FCA compliance, strengthen customer due diligence, and reduce exposure to money laundering risks and compliance penalties.

Use Binderr for AML checks, screen customers against sanctions lists, PEP databases, and adverse media sources using Binderr AML screening tools designed for faster compliance reviews and stronger fraud prevention.

Step 4: Perform Risk Assessment

Risk assessment is a critical stage in the UK KYC compliance process where businesses evaluate customer risk levels based on financial activity, geographic exposure, transaction behaviour, industry type, and onboarding information. Customer risk scoring helps regulated businesses identify low-risk, medium-risk, and high-risk customers while strengthening AML compliance, fraud prevention, and ongoing monitoring processes.

Businesses use risk-based compliance frameworks to assess exposure to money laundering, terrorist financing, sanctions risks, and suspicious activity. Geographic risk analysis, customer behaviour reviews, source of funds checks, and industry-based risk profiling help compliance teams make informed onboarding decisions and determine whether enhanced due diligence is required.

Advanced compliance systems use automated risk scoring models, AI-powered analytics, and real-time monitoring tools to improve customer risk assessments and reduce manual compliance workload. Risk-based onboarding also helps businesses prioritize high-risk customer reviews and strengthen regulatory compliance operations.

Step 5: Apply Enhanced Due Diligence if Required

Enhanced Due Diligence (EDD) is required when businesses onboard high-risk customers, politically exposed persons (PEPs), customers from high-risk jurisdictions, or businesses operating in sectors with increased money laundering risks. EDD strengthens UK KYC compliance by requiring additional verification checks, deeper financial reviews, and continuous monitoring procedures.

Businesses conducting enhanced due diligence may request additional identity documents, source of wealth evidence, source of funds verification, transaction history records, corporate ownership structures, and detailed business activity information. High-risk onboarding cases often require senior compliance approval and more frequent customer reviews to reduce AML and fraud risks.

Modern compliance platforms automate enhanced due diligence workflows using AI-powered AML screening, risk scoring systems, adverse media monitoring, and ongoing compliance monitoring tools. Automated EDD processes help businesses improve onboarding efficiency while maintaining strong regulatory compliance standards.

Explore Free Binderr EDD Report Generator Tool

Step 6: Approve and Monitor Customers

Once identity verification, AML screening, customer due diligence, and risk assessments are completed, businesses can approve customers and activate ongoing monitoring workflows. Customer approval decisions are based on onboarding risk levels, AML screening results, compliance reviews, and internal risk management policies.

Ongoing monitoring is a key part of UK KYC compliance because customer risk profiles, sanctions exposure, transaction behaviour, and financial activity can change over time. Businesses must continuously monitor customers for suspicious transactions, sanctions list updates, adverse media findings, and unusual account activity to maintain AML compliance and reduce financial crime risks.

Automated ongoing monitoring systems use real-time alerts, AI-powered transaction monitoring, behavioural analytics, and periodic KYC refresh workflows to improve compliance operations and reduce manual review burdens. Continuous monitoring also helps businesses identify emerging fraud risks, maintain FCA compliance, and strengthen customer risk management.

Automate UK KYC Compliance with Binderr

Manual onboarding and fragmented compliance checks can slow down customer acquisition and increase compliance risks.

With Binderr, you can;

- AI-powered identity verification for secure customer onboarding workflows

- AML and sanctions screening for high-risk customer compliance checks

- Real-time onboarding checks with automated fraud detection systems

- Continuous monitoring alerts for suspicious activity and risk changes

- Faster customer onboarding with automated identity verification processes

- Audit-ready compliance workflows for FCA and AML reporting requirements

Penalties for Non-Compliance with UK KYC Regulations

Weak KYC compliance controls, poor AML screening, and ineffective customer due diligence processes can expose businesses to FCA investigations, compliance penalties, reputational damage, and financial crime risks in the UK. Inadequate identity verification, sanctions screening, and ongoing monitoring frameworks may also increase fraud risks and operational challenges.

Businesses that fail to maintain strong UK KYC compliance programs may face licence suspension risks, criminal liability exposure, and increased AML audit scrutiny. Strong customer verification, transaction monitoring, and risk-based compliance processes are essential for reducing regulatory and financial risks in 2026.

FCA regulatory enforcement measures

The FCA can take strict regulatory action against businesses that fail to maintain strong UK KYC compliance, AML screening, customer due diligence, and ongoing monitoring controls. Regulatory investigations, enforcement notices, remediation programs, and operational restrictions can significantly impact regulated businesses, fintech companies, payment providers, and financial institutions.

Weak identity verification processes, poor sanctions screening, inadequate fraud prevention controls, and ineffective AML compliance frameworks may trigger FCA investigations and increased compliance scrutiny.

Monetary fines and compliance penalties

Businesses that fail to meet UK AML regulations and FCA compliance requirements may face substantial financial penalties for weak customer verification, poor transaction monitoring, ineffective sanctions screening, and inadequate customer due diligence procedures. AML and KYC compliance failures can also increase legal costs, operational expenses, and reputational risks.

Large compliance fines often result from weak onboarding controls, failure to report suspicious activity, poor ongoing monitoring, and ineffective financial crime prevention systems.

Regulatory licence suspension or revocation

Serious KYC compliance failures can lead to regulatory licence suspension, onboarding restrictions, or complete licence revocation for regulated businesses operating in the UK. FCA enforcement actions may prevent businesses from onboarding customers, processing transactions, or expanding regulated financial services operations.

Weak AML compliance programs, poor fraud prevention controls, and repeated compliance breaches can significantly affect business continuity, customer trust, and long-term operational growth.

Brand and reputational harm

Poor KYC compliance and AML failures can damage customer trust, investor confidence, and brand reputation across regulated industries. Public regulatory investigations, financial crime exposure, fraud incidents, and compliance failures can negatively impact customer acquisition, business partnerships, and long-term credibility.

Strong customer due diligence, identity verification, sanctions screening, and ongoing monitoring processes help businesses strengthen trust, improve compliance operations, and protect their reputation in highly regulated markets.

Legal and criminal consequences

Businesses that fail to maintain strong UK KYC compliance, AML screening, customer due diligence, and suspicious activity monitoring processes may face serious legal and criminal consequences. Regulatory breaches linked to money laundering, fraud prevention failures, sanctions violations, and weak onboarding controls can expose businesses and compliance officers to criminal investigations, legal penalties, enforcement actions, and financial crime liability.

Failure to report suspicious transactions, conduct proper identity verification, or maintain effective ongoing monitoring controls may also increase exposure to legal disputes, regulatory scrutiny, and operational risks. Strong AML compliance frameworks and risk-based compliance processes help businesses reduce legal exposure and strengthen financial crime prevention controls.

Business and operational limitations

Weak KYC compliance controls and repeated AML compliance failures can result in onboarding restrictions, delayed customer approvals, operational disruptions, and increased compliance remediation requirements. FCA investigations and regulatory enforcement actions may limit a business’s ability to onboard customers, expand services, process transactions, or operate within regulated financial sectors.

Businesses may also face increased compliance costs, additional reporting obligations, and internal remediation programs designed to strengthen identity verification, customer due diligence, AML screening, and fraud prevention frameworks.

Increased AML audit and investigation exposure

Businesses with weak customer verification, poor transaction monitoring, ineffective sanctions screening, and inadequate ongoing monitoring controls may face increased AML audit scrutiny and regulatory investigations. FCA reviews, compliance audits, and financial crime investigations often focus on onboarding controls, suspicious activity reporting, customer due diligence procedures, and AML compliance effectiveness.

Strong KYC compliance frameworks, audit-ready compliance records, automated AML monitoring systems, and secure onboarding workflows help businesses improve regulatory readiness, reduce compliance gaps, and respond more effectively to AML investigations and regulatory reviews.

Try Free AML and KYC Screening Tools with Binderr

Industries Facing the Highest UK KYC Compliance Risks

High-risk industries face stricter UK KYC compliance requirements, enhanced due diligence obligations, AML screening, ongoing monitoring, and stronger identity verification controls due to increased exposure to fraud, money laundering, sanctions risks, and suspicious financial activity.

FCA compliance requirements and customer due diligence regulations are especially important for sectors handling cross-border payments, digital assets, and remote onboarding.

- Crypto and digital assets - Crypto exchanges and digital asset businesses face strict UK KYC compliance, AML screening, wallet monitoring, and enhanced due diligence requirements due to high fraud, sanctions, and money laundering risks. Strong identity verification, source of funds checks, and transaction monitoring are essential for secure crypto onboarding.

- Gambling and gaming - Gambling and gaming businesses face increased fraud, identity theft, and money laundering risks linked to high-volume transactions and remote onboarding. Strong customer verification, AML screening, transaction monitoring, and fraud prevention controls help maintain regulatory compliance.

- Forex and trading platforms - Forex brokers and trading platforms manage high-risk financial activity, cross-border payments, and rapid onboarding processes. Strong AML compliance, sanctions screening, identity verification, and customer due diligence controls are critical for reducing fraud and suspicious transaction risks.

- Money service businesses - Money service businesses (MSBs) face elevated UK KYC compliance risks due to international payments, remittance services, and exposure to high-risk jurisdictions. Strong AML monitoring, sanctions screening, and enhanced due diligence frameworks help reduce financial crime risks.

- Payment processors - Payment processors manage large transaction volumes and digital onboarding workflows, increasing exposure to fraud and financial crime. Automated KYC verification, AML screening, transaction monitoring, and AI-powered fraud prevention help strengthen secure payment operations.

- High-risk fintechs - High-risk fintech companies handling digital wallets, embedded finance, and API-driven financial services require scalable KYC compliance infrastructure, automated AML screening, and ongoing monitoring tools to support secure customer onboarding and fraud prevention.

- Wealth management firms - Wealth management firms face stricter enhanced due diligence obligations due to high-value transactions and investor onboarding risks. Source of wealth checks, AML screening, PEP screening, and ongoing monitoring are essential for regulatory compliance.

- Cross-border financial services - Cross-border financial service providers face increased sanctions risks, international onboarding challenges, and global AML compliance obligations. Strong customer verification, transaction monitoring, enhanced due diligence, and ongoing AML monitoring help maintain secure international operations.

Common UK KYC Compliance Challenges to Avoid

Rising fraud risks, stricter AML regulations, and faster digital onboarding are creating new UK KYC compliance challenges for regulated businesses in 2026. Managing identity verification, AML screening, sanctions checks, customer due diligence, and ongoing monitoring efficiently is becoming critical for secure and compliant onboarding.

The following challenges can increase fraud risks, onboarding delays, compliance costs, and regulatory exposure if businesses lack strong KYC verification and AML compliance controls.

Managing false positives in AML screening

Problem: Poor AML screening systems often generate excessive false positives, increasing manual compliance reviews, onboarding delays, and operational workload for regulated businesses. Weak sanctions screening and outdated matching algorithms can slow customer onboarding and reduce compliance efficiency.

Solution: Businesses can reduce false positives by using AI-powered AML screening, smart matching algorithms, risk-based screening workflows, and automated ongoing monitoring systems. Advanced compliance tools improve sanctions screening accuracy, strengthen customer due diligence, and support faster onboarding.

AI-powered AML screening platforms help compliance teams reduce false positives, review sanctions matches faster, and improve ongoing monitoring efficiency.

Use Binderr compliance and AML monitoring tools to manage sanctions screening, suspicious activity reviews, and ongoing customer risk monitoring more efficiently.

Handling international customers

Problem: Cross-border onboarding creates UK KYC compliance challenges linked to international document verification, sanctions compliance, language barriers, and high-risk jurisdiction exposure. Businesses onboarding global customers may face increased fraud risks and enhanced due diligence requirements.

Solution: Using global identity verification systems, automated AML screening, multilingual onboarding workflows, and real-time sanctions checks helps businesses strengthen cross-border compliance operations and improve secure international onboarding.

Verifying remote identities securely

Problem: Remote onboarding increases exposure to identity theft, synthetic identities, fake documents, and deepfake fraud. Weak biometric verification and poor identity authentication systems can create serious AML compliance and fraud prevention risks.

Solution: Businesses can strengthen remote identity verification using biometric authentication, liveness detection, OCR document verification, facial recognition, and AI-powered fraud detection systems. Secure digital onboarding workflows help reduce onboarding fraud and improve customer verification accuracy.

Keeping up with changing regulations

Problem: Evolving FCA compliance requirements, AML regulations, sanctions updates, and customer due diligence expectations make it difficult for businesses to maintain fully compliant onboarding and monitoring processes.

Solution: Automated compliance platforms, real-time regulatory updates, risk-based compliance workflows, and ongoing AML monitoring systems help businesses adapt quickly to changing UK KYC compliance requirements and strengthen audit readiness.

Managing ongoing monitoring requirements

Problem: Continuous transaction monitoring, sanctions screening updates, customer reviews, and suspicious activity detection can create a heavy operational burden for compliance teams managing large customer volumes.

Solution: Automated ongoing monitoring systems, AI-powered transaction monitoring, real-time compliance alerts, and risk-based customer reviews help businesses improve AML compliance efficiency while reducing manual compliance workload.

Preventing onboarding fraud and deepfakes

Problem: AI-generated fraud, synthetic identities, fake documents, and deepfake attacks are increasing risks during digital onboarding and customer verification processes. Weak identity verification controls may expose businesses to financial crime, fraud losses, and compliance failures.

Solution: Businesses can reduce onboarding fraud risks using biometric verification, liveness detection, AI-powered fraud prevention, document authentication, and advanced identity verification technologies. Strong KYC verification frameworks improve secure onboarding and strengthen AML compliance operations.

Get Complete UK KYC Compliance Solution with Binderr

- KYC and KYB verification for regulated businesses

- AML screening and monitoring with ongoing risk checks

- UBO identification and ownership structure verification workflows

- Dynamic risk scoring for customer due diligence processes

- Workflow automation for faster onboarding and compliance operations

- Real-time compliance alerts for suspicious activity monitoring

- Audit-ready reporting for FCA and AML compliance reviews

- API-based integrations for scalable onboarding and verification systems

Bottom Line

UK KYC compliance is becoming increasingly important for businesses managing digital onboarding, customer due diligence, AML screening, sanctions checks, and ongoing monitoring in 2026. Strong identity verification, fraud prevention, transaction monitoring, and risk-based compliance frameworks help regulated businesses reduce financial crime risks, improve onboarding security, and meet FCA compliance requirements.

AI-powered compliance infrastructure, automated AML screening, biometric verification, and real-time monitoring systems are helping businesses improve compliance efficiency while reducing onboarding delays and manual compliance workload. Businesses looking to streamline KYC verification, AML compliance, and onboarding automation can use Binderr Compliance to strengthen secure and scalable compliance operations.